Qualcomm (NASDAQ:QCOM | QCOM Price Prediction) just had one of its most violent single-day reversals of the year, and the question on every shareholder’s mind is whether $228.99 can become $300 before the calendar flips. Based on our proprietary model, the answer is yes, though the path will be volatile.

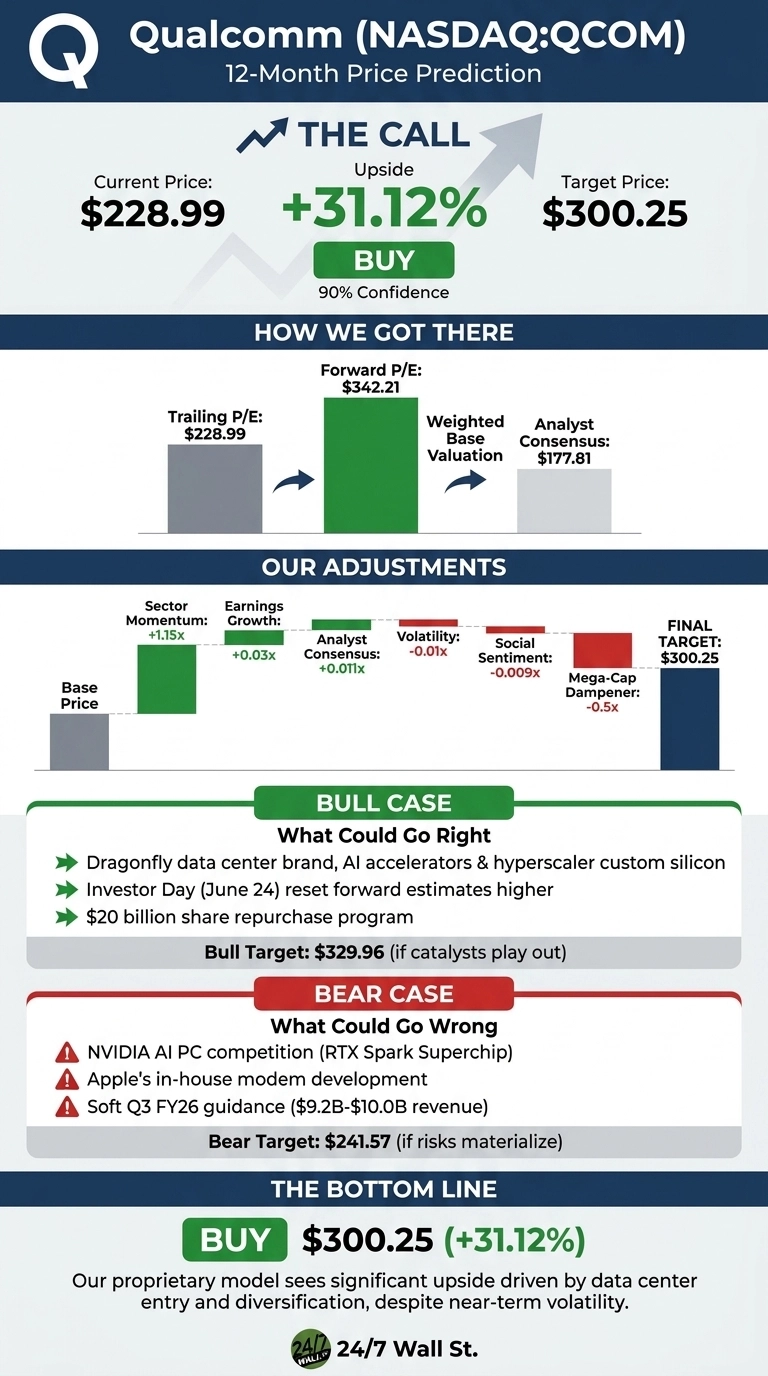

Our 24/7 Wall St. price target for QCOM stock is $300.25, implying 31.12% upside over the next 12 months. We rate QCOM a buy with 90% confidence, the higher end of our conviction scale.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $228.99 |

| 24/7 Wall St. Price Target | $300.25 |

| Upside | 31.12% |

| Recommendation | BUY |

| Confidence Level | 90% |

From Record High to Computex Shock in One Session

QCOM closed June 1 at $228.99, down 8.78% on the day after NVIDIA (NASDAQ:NVDA) used Computex to launch the RTX Spark Superchip at 100+ TOPS against Qualcomm’s Snapdragon X Elite at 45 TOPS. Microsoft (NASDAQ:MSFT) also reportedly eased Copilot+ PC hardware exclusivity, removing a structural tailwind. Despite that, QCOM is still up 34.74% YTD and 61.4% over one year, sitting 32% below its 52-week high of $259.92.

Fundamentals remain intact. Q2 FY26 delivered Non-GAAP EPS of $2.65 against a $2.556 consensus, the fourth straight EPS beat. Automotive set a record at $1.326 billion, up 38% YoY, and IoT grew 9%, offsetting a 13% handset decline tied to memory supply constraints.

The Case for $330 and Beyond

Our bull case targets $329.96 by June 2027, a 44.09% return. The setup hinges on three catalysts. First, the new Dragonfly data center brand, with AI200 and AI250 accelerators, a Humain supply agreement, and a ByteDance ASIC shipment in 2026, opens a multi-billion dollar revenue stream by fiscal 2027.

Second, CEO Cristiano Amon confirmed “a leading hyperscaler custom silicon engagement is on track for initial shipments later this calendar year.” Third, the June 24 Investor Day on Data Center and Physical AI could reset forward estimates higher. CFRA maintains a Buy, and capital return remains aggressive with a $20 billion repurchase authorization.

The Risks Worth Watching

Our bear case puts QCOM at $241.57 a year from now, only 5.49% above current levels. NVIDIA’s Computex push into AI PCs is the clearest near-term threat, and Apple (NASDAQ:AAPL)’s in-house modem development continues to eat at Qualcomm’s most lucrative socket.

Q3 FY26 guidance was soft at $9.2 billion to $10 billion in revenue with EPS of $2.10 to $2.30. Bulls would counter that management explicitly flagged Q3 as the handset bottom with sequential recovery in Q4, and that the GAAP net loss noise in Q4 FY25 came from a $5.7 billion non-cash tax charge tied to new legislation.

The street consensus target of $177.81 sits well below today’s price, meaning analysts as a group see downside risk our model does not.

Qualcomm Price Prediction 2026-2030

The bull thesis at $228.99 rests on the Investor Day on June 24 putting firm numbers behind Dragonfly and the hyperscaler custom silicon ramp. The bear thesis rests on NVIDIA’s AI PC push structurally eroding Snapdragon X share before data center revenue can scale.

My read is that the diversification story is real, the buyback is real, and the panic on June 1 was an overreaction. The 24/7 Wall St. price target stands at $300.25 with a buy rating and 90% confidence.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $275.32 |

| 2027 | $300.25 |

| 2028 | $355 |

| 2029 | $420 |

| 2030 | $497.07 |

These projections assume Qualcomm continues executing on data center entry and automotive scale. Significant upside or downside could result from Apple’s modem timeline and the pace of hyperscaler AI silicon adoption.

Contact [email protected] for any questions or corrections.